Our journey discussing the benefits of auditing organizational culture is coming to an end. We began this series by introducing initial cultural auditing concepts in the first article. Then, in the second article, we continued by more closely examining the first half of the top ten tips that were outlined. In this, the final article of the series, we wrap up with the second half of that list and conclude our analysis.

Auditing culture

Auditing culture requires involving a wide range of stakeholders and will require you to consider alignment of the desired culture to the actual activities of many people. As we have seen, the leadership in the organizations and the people within the business are clearly very important. To get a true sense of culture you will also need to consider organizational partners and outside service suppliers.

If culture is the way things are done more informally, then this impacts everything in your entire organization’s wider sphere. In this context, procurement may be an important stakeholder to engage with in any cultural audit to better understand their selection methodologies, allowing you to form a view, for example, on how they consider cultural fit in the selection of any third-party suppliers. It also goes beyond the selection of suppliers to how we treat them once they are in place. Does the organization treat them fairly, or is the focus on cost at the expense of other, more important matters?

Ensure that you consider both design and operating effectiveness

Auditing work should be examining both design and operating effectiveness. Cultural reviews are no different but have the tendency to focus on design at the cost of operating effectiveness. As with all audit work, you would typically begin with a risk and control assessment which can be developed in line with the cultural levers you have identified. Typically, an auditor would then request documents, allowing some desktop analysis ahead of the interviews. Interviews with management can focus on whether they understand the desired culture and can clearly articulate this, while also identifying which levers they see as being particularly important for ensuring the culture is real and lived on the front line. Interviews should also probe the extent to which management role model the desired culture every day and ensure their teams’ activities are in line with the culture.

However, understanding operating effectiveness requires a wider approach and talking to a wider range of employees. Focus groups or surveys can be effective to gather data from employees and may provide more diverse views. If focus groups are operated, they will require additional skill, with the lead needing to manage the group so that a fair range of positive and negative views are heard.

Despite the limitations of cultural measures these too should be requested for each of the levers to understand the extent to which the organization has cultural measures and whether the results are acted upon. Measures that you may wish to consider typically involve people management activity, such as employee turnover, exit interview data, grievances raised by employees, whistleblowing information, and absence data. Other areas should also be explored, such as customer complaints data. However, collecting these may present a challenge. If culture is important in the organization, then it will be available and likely reviewed. If not, there is the potential your first audit finding on the need for management to have appropriate measures in place to track whether the desired culture is being delivered in practice.

In my experience, there is no, single best way of conducting cultural audits. Rather, you need to form a view of what is right for your organization. One aspect you will need to consider is whether you conduct specific cultural reviews in your audit plan, have it as a component in all audits that you conduct, or draw out cultural consideration into an off-plan piece of work. I’ve seen all aspects of all three of the options successfully implemented.

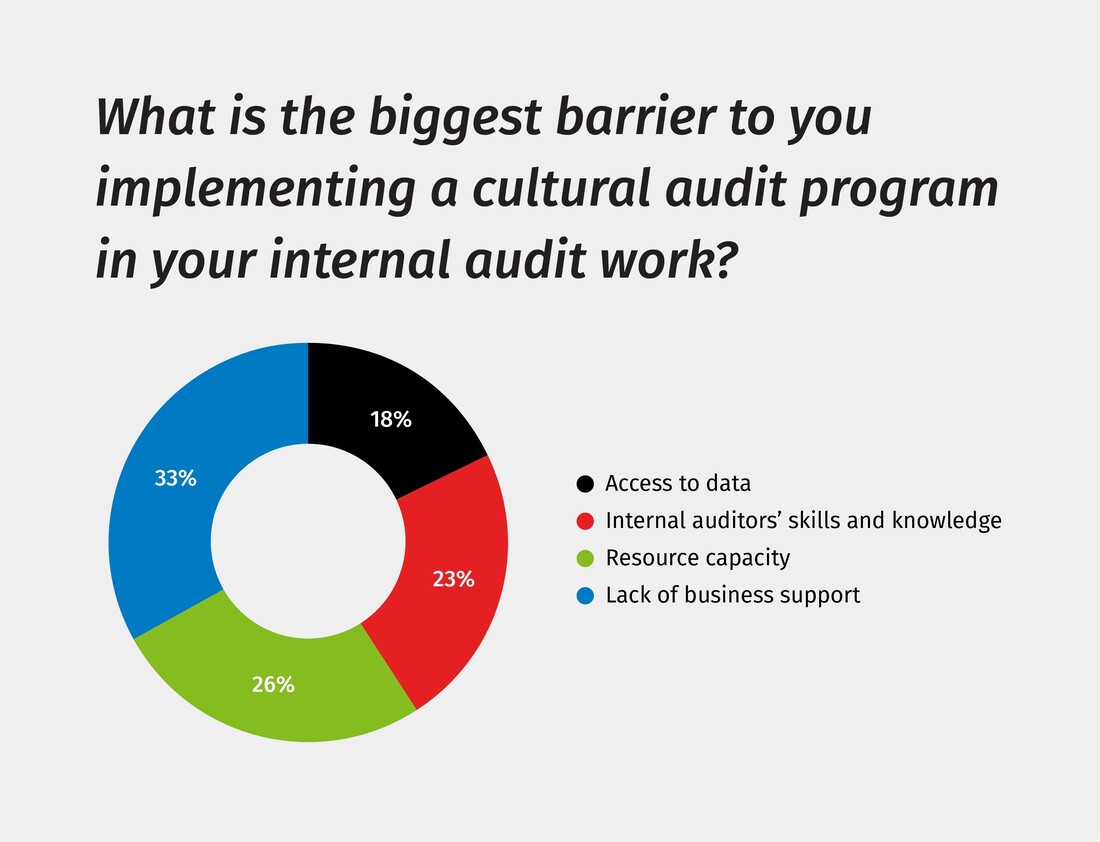

We asked 2000 internal audit professionals during a recent webinar – “What are the biggest barriers to you implementing a cultural audit program in your internal audit work?” The results demonstrated the following:

Don't go for a grand plan

It is important that you consider how you introduce cultural auditing into your program of work. It’s a sensitive topic, and management will often be wary of audit getting too involved. Your internal audit colleagues may also be nervous about whether an area like culture can, in fact, be meaningfully audited. The best advice being — don’t go for a grand plan, but rather start small, test, and learn as you go. This includes building support from the Board and executive leadership by demonstrating, as you go, the insights gained from the cultural examination you have completed and the possibilities to go further with increased resources and business buy-in to this challenging area.

This lends itself to the suggestion to start with a pilot, or a proof of concept, where you identify an area of the business to work with and look to introduce the concept of auditing culture at this point. This should be an area where you know you have a senior auditee who is an advocate of internal audit and willing to work with you to make the pilot a success. I have found that success breeds more success and considerable momentum can be delivered in this manner. Early on, it is also good to share examples of your work and the value it is bringing. I call this the “test, share, and impress approach.”

Collaborate with your business colleagues

It is also very important to work with the business. The tip here being: Collaborate with your business colleagues – independence is a mindset. I have spent time with many auditors who have been reluctant to collaborate in any deep manner with the business, citing the audit charter and the need for full independence from first-and-second-line activity. I agree, our independence as internal auditors is very important. We need to be objective in all we do to avoid threatening this. However, I don’t believe independence means that we cannot work closely with the business where it makes sense to do so.

One such area, for example, is the identification of the cultural levers discussed earlier – an organization-wide conversation on this is helpful in building appropriate understanding and support for the examination you wish to conduct. Also important is the identification and quick access to relevant data for your cultural work, both at an organization-wide level, but also in divisional units of your business. There is likely to be shared interest in this area, particularly with your HR function. Given this shared interest, it makes sense for all those interested in cultural understanding to come together to share ideas and data for the benefit of the business. For example, this may mean developing a shared data area that all can access. Identify across your business who is interested in this space and join with them to share, learn, and progress.

Upskill all auditors at all levels

Finally, ensure that the program of work you want to introduce is a sustainable approach to auditing culture. Find a way to get your people behind this approach. At heart, we are a people business and any push to audit this challenging area on a sustainable and systematic basis will depend on the skills and knowledge of your teams.

This leads to the final tip to upskill all auditors at all levels. As we identified earlier, your impact is likely to be much higher if your teams integrate consideration of cultural levers and impacts throughout your audit work and not just in any standalone audit you may do. Understanding the nuances of culture is not simply reserved for HR and psychologists but is a core competency for all auditors. This should be reflected in the recruitment and development approach for your team.

This is likely to mean that if you are going to make cultural assessment a core part of your internal audit work you will need to provide training to the audit team. This will need to cover the organizational cultural levers that you have identified, the data that can help you understand these levers, and the interviewing techniques that will need to be employed to get to actual, as well as espoused, culture. Be honest with yourself and acknowledge where you don’t have the skills that are needed. You will likely need to draw on other sources of expertise, including business and external consultancy support. These can allow you to supplement both the capacity and capability of your team.

And, of course, think carefully about how you organize to deliver this challenging area of work. My current view is that a multidisciplinary (sometimes called Hybrid) approach is most successful. This is all about how you set up your operating model to deliver your cultural audit work. Some larger functions have established dedicated, well-resourced teams to examine culture in their organization and have staffed this with a blend of expertise, including behavioral psychologists. This group of specialists work alongside and coach front-line auditors who are then encouraged to consider cultural levers in all their audit work as we discussed earlier. Clearly, this is more relevant for larger organizations, but even in smaller functions, you may choose to appoint a cultural lead (or champion) with the responsibility to support and drive the integration of cultural aspects into all your audit work.

Conclusion

There is no silver bullet for the successful development and implementation of a cultural audit program. Hopefully, the tips that were provided throughout this series of articles will be a useful catalyst for your work in this space as you consider the conditions needed for you to achieve momentum around the idea of auditing culture in your organization.