Auditing organizational culture is a challenging area for internal audit. Culture is dynamic, and regularly changing. Successful auditing of culture requires a holistic approach across the internal audit function covering the development of internal auditor skills, adjustment to audit methodology, and buy-in from the business regarding the value insightful culture auditing can bring.

In this first article of a three-part series, we examine and discuss the various factors for successfully auditing and influencing culture in your organization.

What is organizational culture, and why does it matter?

Before looking at how you audit culture, it’s necessary to first have a good understanding of what you mean by culture and why it’s important to organizational success.

The classic definition is around the phrase coined by Charles Handy, “the way things are done around here”. While helpful for us to gain insights into auditing culture, we need to unpack this further. Culture is about the interaction between values and behaviors and how these are seen in the organization’s activities and interactions with the range of stakeholders it has (e.g., employees, customers, suppliers, and society).

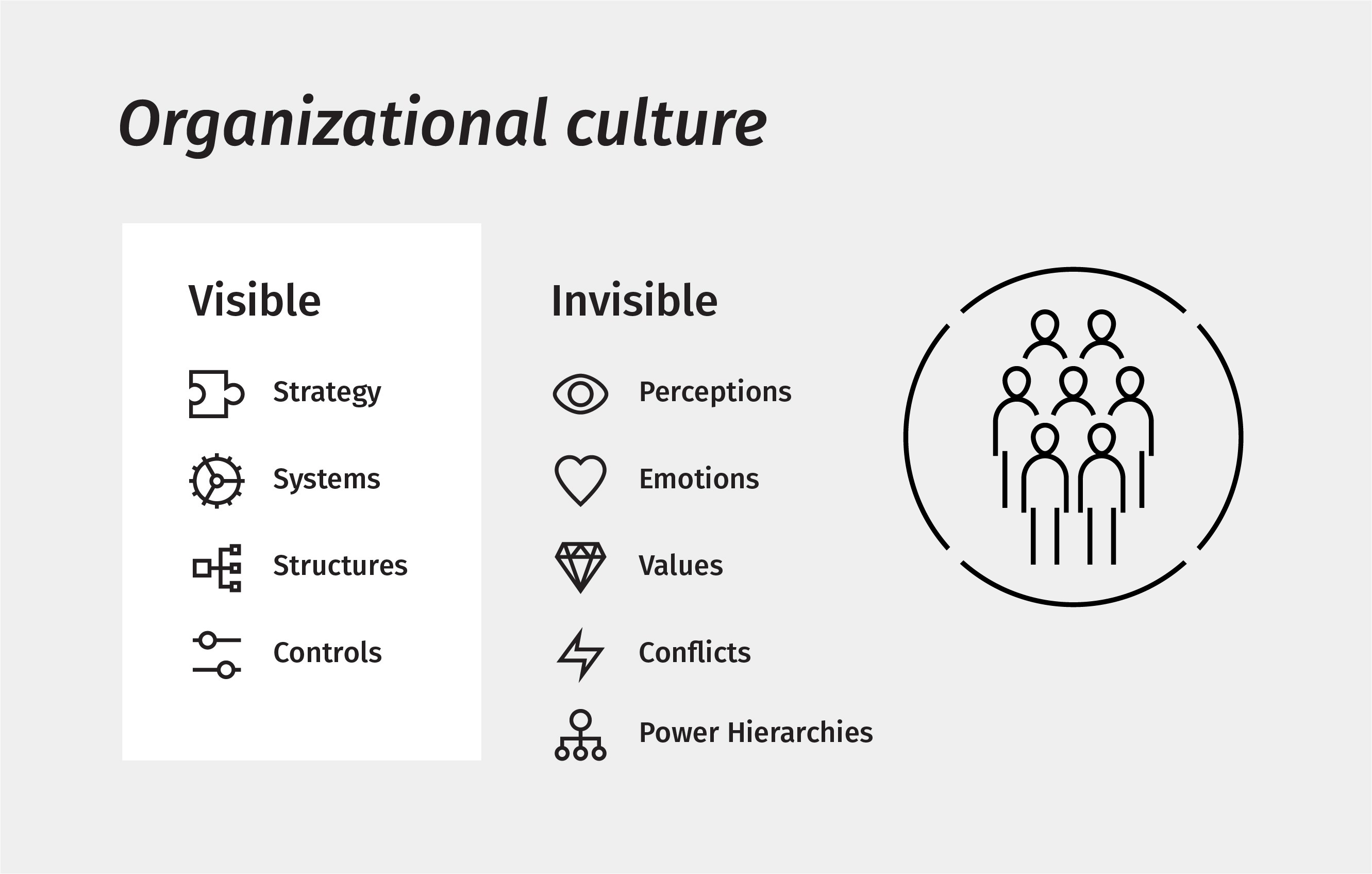

Much of what goes on in an organization is hidden and informal. On the left side of the Organizational Culture graphic, you see some of the more formal or visible aspects of an organization – that is its systems, structures, controls, and strategy. These are largely defined and controllable. But, arguably more important, are the invisible or informal properties that are present in every organization. These include the perceptions, emotions, values, conflicts, and power hierarchies in place that are shaped by every interaction each day. These aspects have an incredible effect on an organization and their influence often overrides the more formal structures that sit in clear view. Therefore, when we evaluate culture, it requires looking beyond the formal processes and controls.

The structured approach auditors take to their work, and the focus they take on hard data and processes could mean that those ‘invisible’ aspects of culture are not appropriately considered. However, many internal audit functions are now starting to develop their work to closely examine these areas and form a needed opinion. In doing so, it is important that we do not lose the rigor in our work by simply using gut feeling in our audits of culture. We need to make use of both hard and soft indicators to manage subjectivity in our findings. Data is key to identifying patterns in how the organization is behaving with colleagues, customers, and suppliers, to provide insights that benefit the organization and lead to better business outcomes.

Understanding culture and its effect on the business really does matter. Business academic Peter Drucker once said, “Culture eats strategy for breakfast”. Big failures, something we in internal audit are keen to help avert in our control assessment work, are often cultural. In this context, organizational culture matters to us in internal audit as we see that having the right corporate culture is crucial to the sustainability and resilience of an organization. If we do not have an opinion on the effectiveness of culture, how can we truly give an opinion on the effectiveness of the internal control environment?

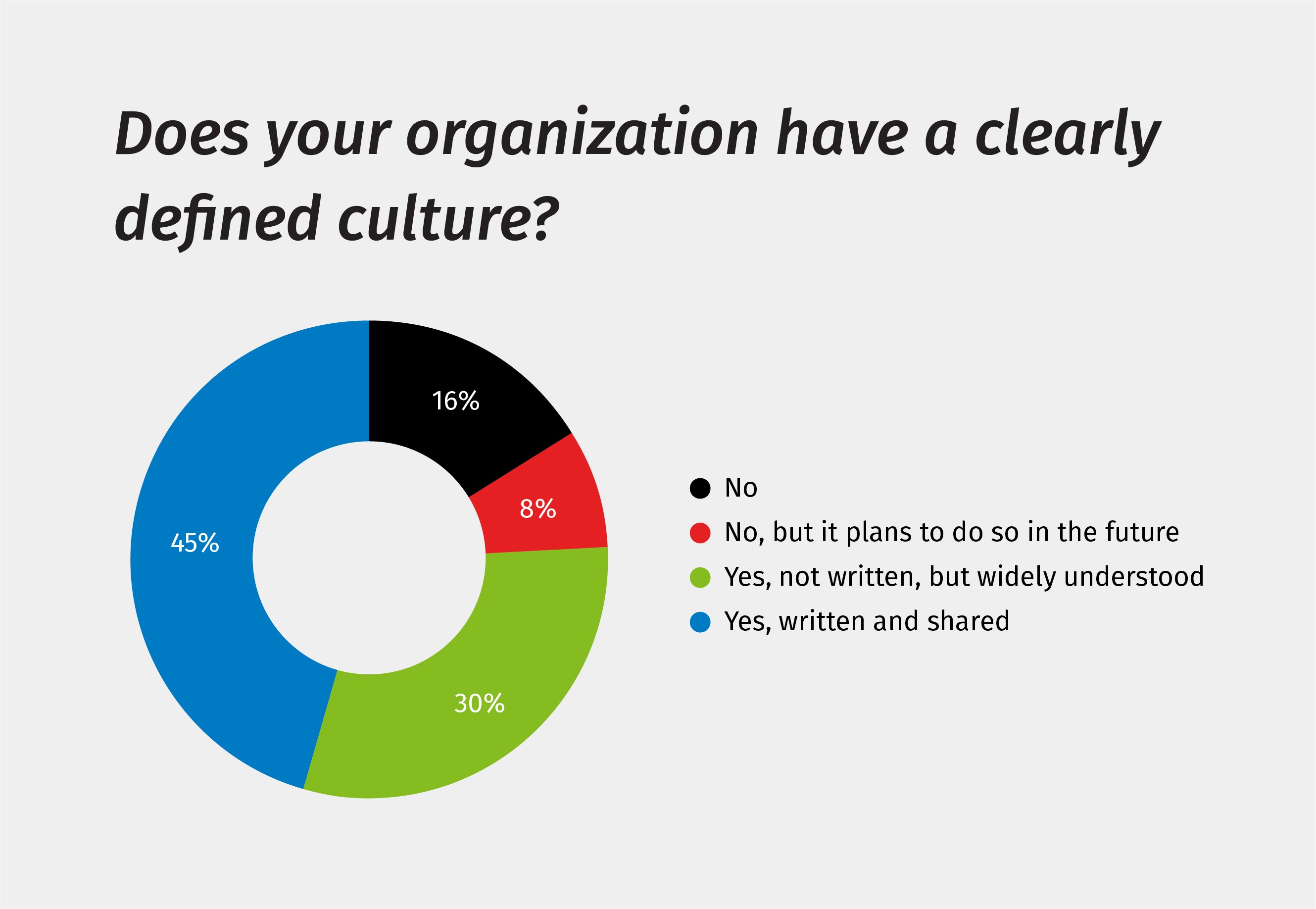

We asked 2000 internal audit professionals during a recent webinar whether their organization has a clearly defined culture. The results showed the following:

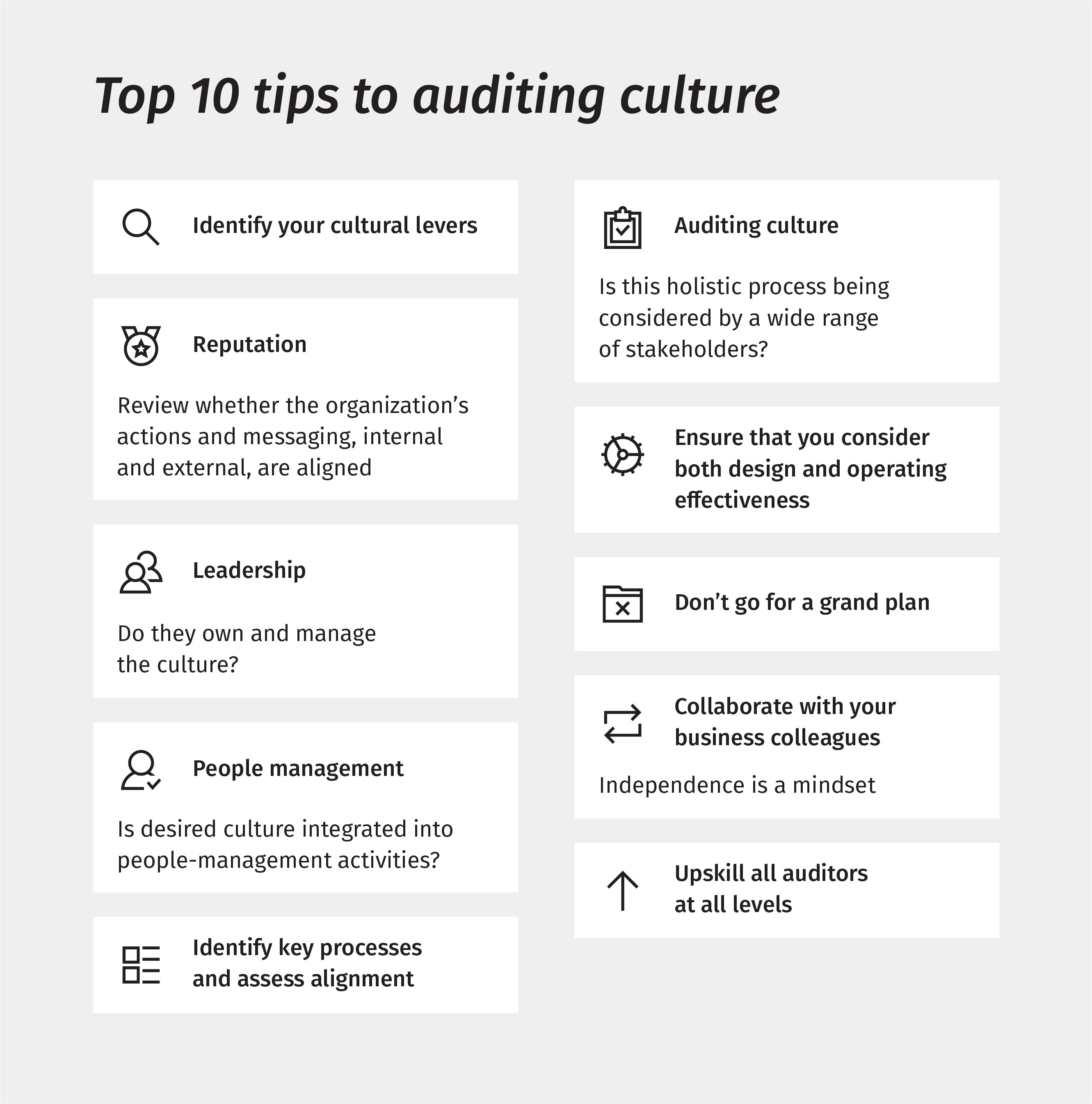

Top ten tips

Given the fact that you are reading this article, hopefully you are already convinced that internal audit has a role to play within the organization when it comes to assessing culture. You may already be on this journey delivering cultural insights through your work to your Board, or you may simply be interested in learning more about how to begin this journey. Whichever stage you find yourself, the following top 10 tips will provide you with some initial and practical thoughts that provide a view on culture and the direction needed to influence both management and the Board.

In the coming second and third articles of this three-part series on auditing culture, we will take a closer look and provide a more in-depth examination of each of these suggested ten tips. These follow-up articles will offer examples and provide opportunities to more successfully audit and influence the culture at your organization.