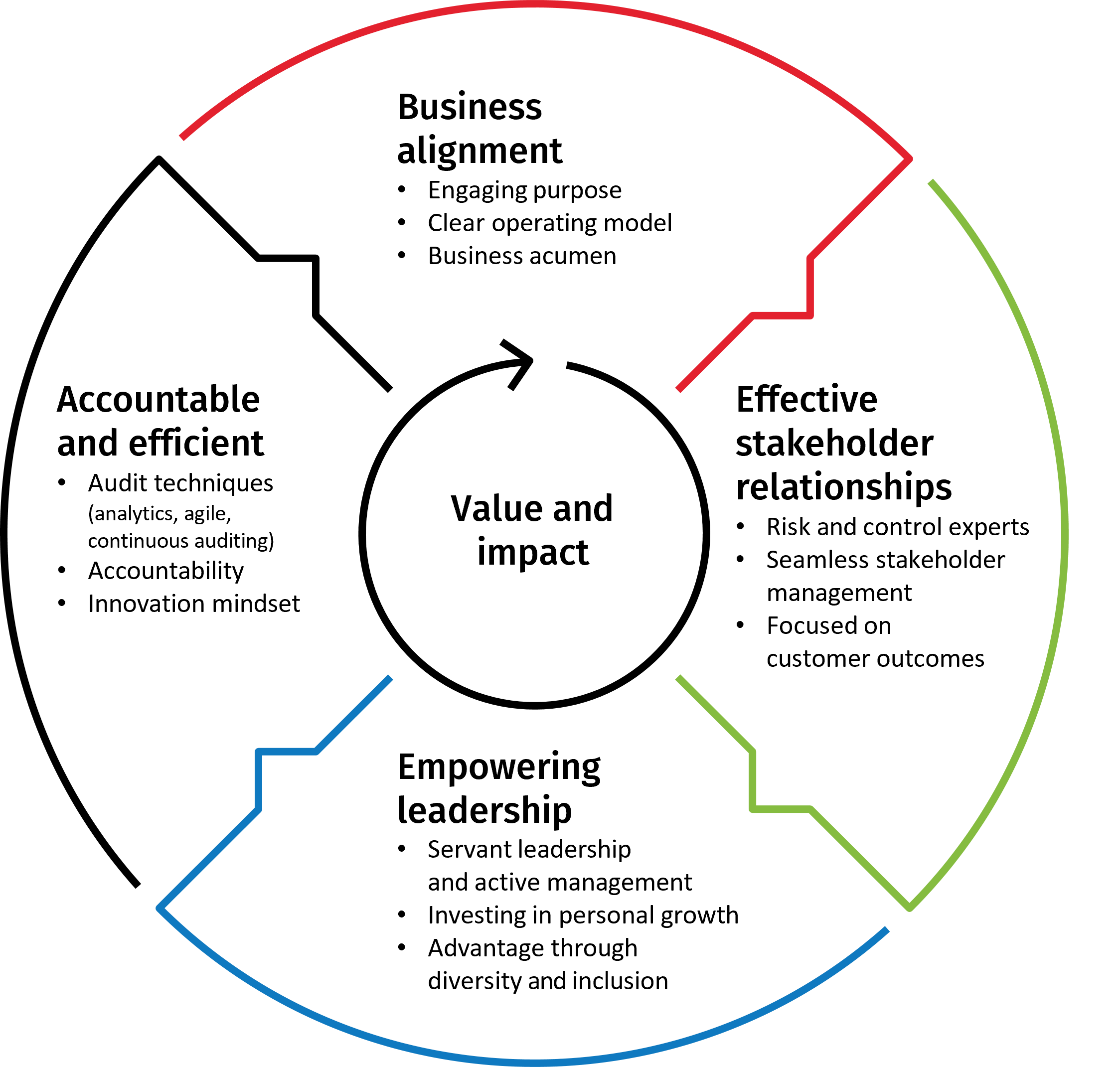

Up to this point we have explored the first three characteristics – business alignment, internal audit stakeholder relationship management, and empowering leadership. And I wanted to personally thank you for sticking with me throughout this journey. In this final installment we explore characteristics #4 – accountable and efficient and its components that include audit techniques, accountability reporting, and what it means to have an innovative mindset.

- Audit techniques – Assurance plus

- Accountability

- Innovative mindset

Audit techniques – Assurance plus

High performance internal audit teams look to deliver value beyond traditional audit work. Internal audit should be the catalyst for management action that makes the business more secure and sustainable by having a constant focus on control improvement. To be successful requires deploying a range of internal audit ‘products’ such that the Internal Audit intervention is optimum for the risk and controls that we are looking to examine. These products typically should include:

- Change assurance – Ongoing audit work alongside business change programs. Auditors in the field alongside the change activity add value throughout the process in real-time.

- Data analytics work – Continually highlighting deficiencies when they occur. Even better if the analytics developed can be handed over to the business so they can own ongoing (and automated) assessment of their controls.

- Business monitoring or continuous auditing – Ongoing risk assessment work. This is an evolution of the audit from point-in-time judgment on controls to ongoing review and insight on the effectiveness of the control environment. This is done by identifying and monitoring key risk indicators that provide warnings of deficiencies as they happen.

- Flash audit work – Internal audit functions that do this type of ‘flash’ audit work are typically not engaged for more than a week. Reporting is often verbal, supported by a one-page memo, and cleared through internal audit sign-offs. Executive leadership values this approach with its pace and immediacy, allowing for quick change in the business and immediate impact. In high performance internal audit functions, auditors also embrace this pace of delivery that focuses on smaller, more targeted scopes.

In this context, high performance internal audit functions will see traditional full-scope audits operating increasingly as a smaller proportion of the overall book of work, completed each year, with these being increasingly accompanied by all the above activities.

Accountability

Just like any other business unit, it is important that the internal audit function is accountable for its performance. High performance teams recognize and welcome this scrutiny to ensure they are continually improving and not becoming complacent. To that end, they report to the Board on their performance on a periodic basis, the frequency being determined by their scale - the larger, the more frequent. This is not the regular reporting of audit findings that is about internal audit holding a mirror up to the business and showing what we see. This is holding the mirror up to ourselves and letting others see what we look like!

To be considered as truly high performing, internal audit functions should submit to the Board an Internal Audit ‘Annual Report’ (and for larger functions, I would expect this type of accountability reporting to be quarterly). Similar to the business, this annual report demonstrates what has happened in the prior year and then looks forward to the year ahead. This is the ideal vehicle to showcase the enhanced value that a high level of performance is bringing and establishes a firm reputation as adding value.